One of the first questions many homebuyers ask is:

“What credit score do I need for a conventional loan?”

If you’re considering buying a home in Charlotte, Fort Mill, Indian Land, Rock Hill, Lancaster, Waxhaw, Matthews, or anywhere throughout North or South Carolina, understanding credit score requirements is an important first step.

Many buyers assume they need perfect credit to qualify for a conventional mortgage. Fortunately, that’s not true.

While conventional loans generally have stricter credit requirements than FHA loans, many borrowers qualify with credit scores that are lower than expected.

At Carolina Mortgage Firm, we help buyers evaluate their credit profile, compare loan options, and determine the best financing solution for their goals.

Let’s take a closer look at how conventional loan credit requirements work.

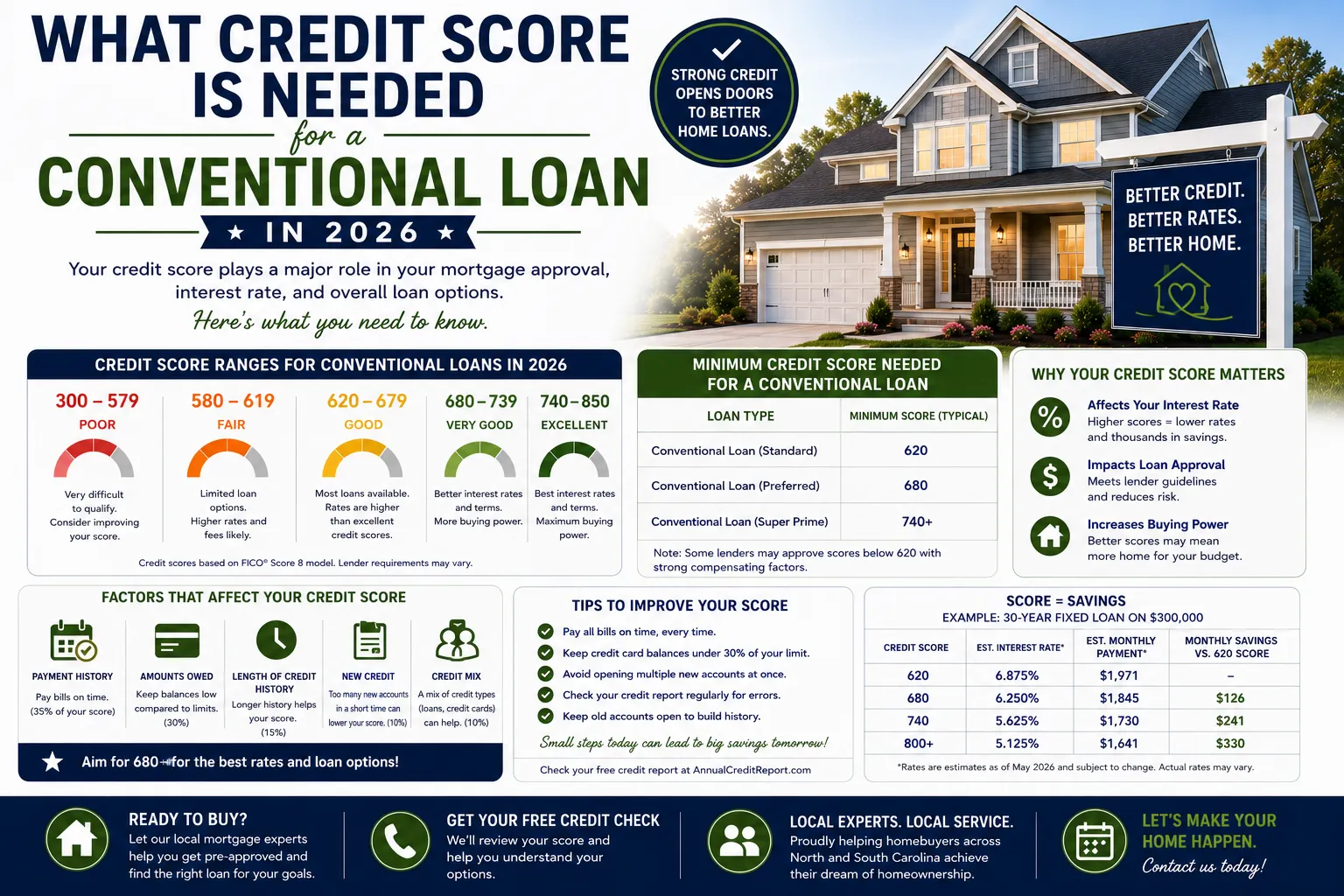

Quick Answer: Conventional Loan Credit Score Requirements

Most conventional loan programs require a minimum credit score of:

620 or Higher

A credit score of 620 is generally considered the minimum for most conventional mortgage programs.

However, qualifying and receiving the best pricing are two different things. Borrowers with higher credit scores often receive:

- Better interest rates

- Lower mortgage insurance costs

- More financing options

- Improved loan terms

The stronger your credit profile, the more options may be available.

What Is a Conventional Loan?

A conventional loan is a mortgage that follows guidelines established by:

- Fannie Mae

- Freddie Mac

Unlike FHA, VA, and USDA loans, conventional mortgages are not government-backed. Because of this, lenders often place greater emphasis on:

- Credit history

- Debt-to-income ratios

- Assets

- Financial reserves

Conventional loans are one of the most popular financing options in the United States.

Why Credit Scores Matter for Conventional Loans

Your credit score helps lenders evaluate risk. The score reflects your history of:

Making Payments On Time

Managing Debt Responsibly Maintaining Credit Accounts Avoiding Delinquencies

While credit scores are important, lenders also consider your overall financial profile.

Mortgage approval is never based solely on a credit score.

Conventional Credit Score Ranges Explained

620–659

Generally meets minimum qualification requirements.

Borrowers may qualify but could see higher interest rates or mortgage insurance costs.

660–699

Often opens additional financing opportunities. May provide more competitive loan terms.

700–739

Considered a strong credit profile. Frequently results in improved pricing.

740+

Often receives the most favorable conventional loan pricing available.

Many buyers are surprised to learn that even small improvements in credit score can create meaningful savings over time.

How Credit Scores Affect Interest Rates

Your credit score directly impacts mortgage pricing. Generally speaking:

Higher Credit Scores

May result in:

- Lower interest rates

- Lower monthly payments

- Reduced mortgage insurance costs

Lower Credit Scores

May result in:

- Higher rates

- Increased monthly payments

- Higher borrowing costs

Over the life of a mortgage, even a small rate difference can save thousands of dollars.

What Credit Score Gets the Best Conventional Loan Terms?

While every lender evaluates risk differently, many borrowers begin seeing the most favorable pricing at:

740 and Above

This doesn’t mean buyers below 740 shouldn’t pursue homeownership.

In many cases, purchasing sooner makes more financial sense than waiting years to achieve a perfect score.

A mortgage consultation can help evaluate your specific situation.

Conventional Loans vs FHA Credit Requirements

Many buyers compare conventional and FHA financing.

FHA Loans

Often provide greater flexibility for lower credit scores.

Conventional Loans

May offer better long-term affordability for borrowers with stronger credit profiles. This is why comparing both options is important.

At Carolina Mortgage Firm, we frequently review both programs to determine which provides the greatest benefit.

Common Credit Issues That Affect Conventional Loans

Late Payments

Recent late payments may impact qualification.

High Credit Card Balances

High utilization can reduce scores.

Collection Accounts

May require additional review.

Bankruptcies

Waiting periods apply.

Foreclosures

Seasoning requirements may exist.

Many of these issues can be addressed with proper planning.

How to Improve Your Credit Score Before Applying

If you’re planning to buy a home within the next year, consider these strategies.

Pay Down Credit Card Balances

Reducing utilization often improves scores.

Make Payments On Time

Payment history remains one of the most important factors.

Avoid Opening New Accounts

New debt can temporarily affect scores.

Monitor Credit Reports

Correct inaccuracies promptly.

Avoid Large Purchases

Preserve your financial profile before applying.

Even modest improvements can strengthen your mortgage application.

Common Conventional Credit Score Myths

Myth #1: You Need Perfect Credit

False.

Many buyers qualify with scores well below 800.

Myth #2: 620 Guarantees Approval

False.

Income, assets, and debt also matter.

Myth #3: Checking My Credit Will Ruin My Score

False.

A mortgage credit inquiry generally has minimal impact.

Myth #4: I Should Wait Until My Score Is Perfect

Not always.

Market conditions, home prices, and personal goals should also be considered.

Other Factors Lenders Review

Even with excellent credit, lenders evaluate:

Income

Stable and documentable income.

Employment History

Consistency matters.

Assets

Funds available for down payment and closing costs.

Debt-to-Income Ratio

Monthly obligations relative to income.

Property Information

The home itself must meet lending guidelines.

A complete pre-approval review provides the most accurate picture.

Why Pre-Approval Matters

Before shopping for homes, obtaining a mortgage pre-approval offers several advantages.

Understand Your Budget

Know exactly what you can afford.

Compare Loan Programs

Evaluate Conventional, FHA, VA, and USDA financing.

Identify Improvement Opportunities

Learn how small changes could strengthen your application.

Shop With Confidence

Present stronger offers when you find the right home.

Many buyers discover they qualify sooner than expected.

Why Work With Carolina Mortgage Firm?

At Carolina Mortgage Firm, we help buyers throughout:

- Charlotte

- Fort Mill

- Indian Land

- Rock Hill

- Lancaster

- Matthews

- Waxhaw

- Belmont

- Huntersville

- Concord

understand their credit profile and compare mortgage options. Because we work with multiple lenders, we can compare:

to identify the best financing strategy for your goals.

Frequently Asked Questions

What Is the Minimum Credit Score for a Conventional Loan?

Typically 620 for most programs.

Can I Buy a House With a 640 Credit Score?

Often yes, depending on the overall application.

Is FHA Easier to Qualify For Than Conventional?

In many cases, FHA offers greater credit flexibility.

What Credit Score Gets the Best Mortgage Rates?

Generally, higher scores receive more favorable pricing.

Should I Get Pre-Approved Before House Hunting?

Absolutely.

Related Conventional Resources

- Can I Buy a Home With 3% Down?

- Can Bonus Income Be Used to Qualify?

- Can Commission Income Be Used for a Mortgage?

- What Are Conventional Loan Limits in 2026?

- How Long Is a Mortgage Pre-Approval Good For?

Ready to Explore Your Conventional Loan Options?

Whether you’re purchasing your first home in Charlotte, upgrading in Fort Mill, relocating to Indian Land, moving to Rock Hill, or buying in Lancaster County, Carolina Mortgage Firm can help you understand your credit profile and determine whether a conventional loan is the right fit.

Contact Carolina Mortgage Firm today for a personalized mortgage consultation and pre-approval.