A Partner Mindset — Built for Carolina Communities

We work in communities where names matter, schools matter, and relationships actually last.

We’re a boutique mortgage broker built for people across the Southeast who value thoughtful guidance, honest communication, and real partnerships.

The Carolinas have always been a place to discover, settle in and live well. We’re here to help you do the same.

We’re a veteran-owned, independent brokerage rooted in North and South Carolina, working alongside clients and partners as they make decisions about where to put down roots next. With thirty years of experience, we advocate for our people — offering expert, local guidance through the Carolina markets we know intimately.

Tagline

Because budgeting apps, side hustles, and skipping avocado toast didn’t magically fix the housing market, this guide exists to explain how mortgages actually work right now.

It’s not a pipe dream. The rules just changed.

The Carolinas don’t work like national markets — and neither do we. Relationships matter more. Local knowledge goes further. And the way deals get done is shaped by the communities they’re in.

We work in communities where names matter, schools matter, and relationships actually last.

What works in one Carolina neighborhood won’t always work a mile away — we know the difference.

When reputations travel, clear communication isn’t optional — it’s how trust is built.

We believe in paying it forward.

That’s why a portion of every loan supports the ROB Foundation, a local nonprofit providing college scholarships to students who have lost a parent. The foundation honors the life of Rob — a friend and member of our extended team — whose passing in 2021 deeply affected our community.

Through this partnership, every closing helps support students as they move toward a future of opportunity.

Salt, sun & easy living

Easy mornings, salty air, and a pace that feels intentional.

For those who believe where you live should shape how you live.

Subtly Refined

This is where opportunity meets lifestyle — with walkable centers, thoughtful development, and a strong sense of momentum

Where mountain living meets four-season appeal.

Secure & Steady

Neighborhoods built for staying put — where schools, community, and everyday life connect naturally.

A place that balances growth with familiarity.

Room to breathe

Where weekends slow down, views open up, and life finds a steadier rhythm.

For people drawn to space, nature, and a sense of quiet purpose.

Independent Spirit

For those drawn to culture, craft, and a mountain backdrop that feels lived-in — not just visited.

Creative, independent, and deeply connected to place.

Coast

Dreaming of waking up near the water? The Carolina Coast offers a lifestyle built around ocean views, beach days, and a relaxed pace of life. Whether you’re searching for a primary home, second home, or investment property, coastal areas provide strong appeal—especially for buyers interested in vacation rentals or long-term appreciation. You’ll find everything from condos with oceanfront views to single-family homes tucked into quiet beach communities. When buying near the coast, it’s important to factor in items like flood zones, insurance, and property usage guidelines. With the right planning, coastal homeownership can be both a lifestyle upgrade and a smart investment. If you’re looking for a blend of scenery, recreation, and opportunity, the coast is one of the most rewarding places to buy in the Carolinas.

High Country

If cooler temperatures and mountain living are calling your name, the High Country offers a distinct lifestyle that’s hard to replicate. Centered around towns like Boone and Blowing Rock, this region is perfect for buyers looking for a second home, vacation property, or even a full-time retreat. You’ll find everything from cozy cabins to luxury homes with long-range views. The High Country is known for its four-season appeal—hiking in the summer, vibrant fall colors, and even skiing in the winter. Buyers should consider factors like elevation, weather, and accessibility, especially during colder months. If you want a home that feels like a getaway while still being a smart investment, the High Country delivers on both lifestyle and value.

Low Country

If charm, history, and a slower pace of life are high on your list, the Low Country offers a truly unique homebuying experience. Known for its coastal marshes, scenic waterways, and timeless architecture, this region—especially around Charleston—blends lifestyle and culture in a way few places can. Buyers are drawn to everything from historic homes to newer communities with modern amenities. The Low Country is ideal for those seeking a relaxed, community-focused environment while still enjoying dining, entertainment, and coastal access. Like other coastal regions, it’s important to consider flood zones and insurance as part of your purchase strategy. If you’re looking for character, beauty, and a true Southern lifestyle, the Low Country is a standout choice.

Mountains

If you’re looking for peace, privacy, and incredible views, the mountain regions of the Carolinas may be the perfect fit. Homes here often offer a true escape—whether it’s a full-time residence, second home, or income-producing rental. Nestled in areas around the Blue Ridge Mountains, buyers are drawn to cabins, custom homes, and properties surrounded by nature. Mountain living comes with a few unique considerations, like road access, elevation, and well/septic systems, but the lifestyle payoff is hard to beat. Cooler temperatures, outdoor recreation, and year-round beauty make this a favorite for those wanting to slow down without sacrificing value. If your goal is space, scenery, and a quieter pace, the mountains offer a compelling place to call home.

Piedmont

Looking for the right balance between convenience and lifestyle? The Piedmont region offers some of the best all-around opportunities for homebuyers in the Carolinas. Centered around cities like Charlotte and Columbia, this area gives you access to strong job markets, top schools, and a wide range of housing options. Whether you’re buying your first home, upgrading, or relocating, the Piedmont offers flexibility—from new construction communities to established neighborhoods with more space. You’re also within a few hours of both the mountains and the coast, making weekend travel easy. For buyers who want affordability, accessibility, and long-term growth potential, the Piedmont is often the smartest place to start.

Our team of loan officers brings experience, local insight, and a genuine commitment to doing right by our clients and partners.

Whether you’re a buyer, investor, or real estate professional, you’ll work directly with people who understand your goals and your market.

This is just placeholder text. Don’t be alarmed, this is just here to fill up space since your finalized copy isn’t ready yet.

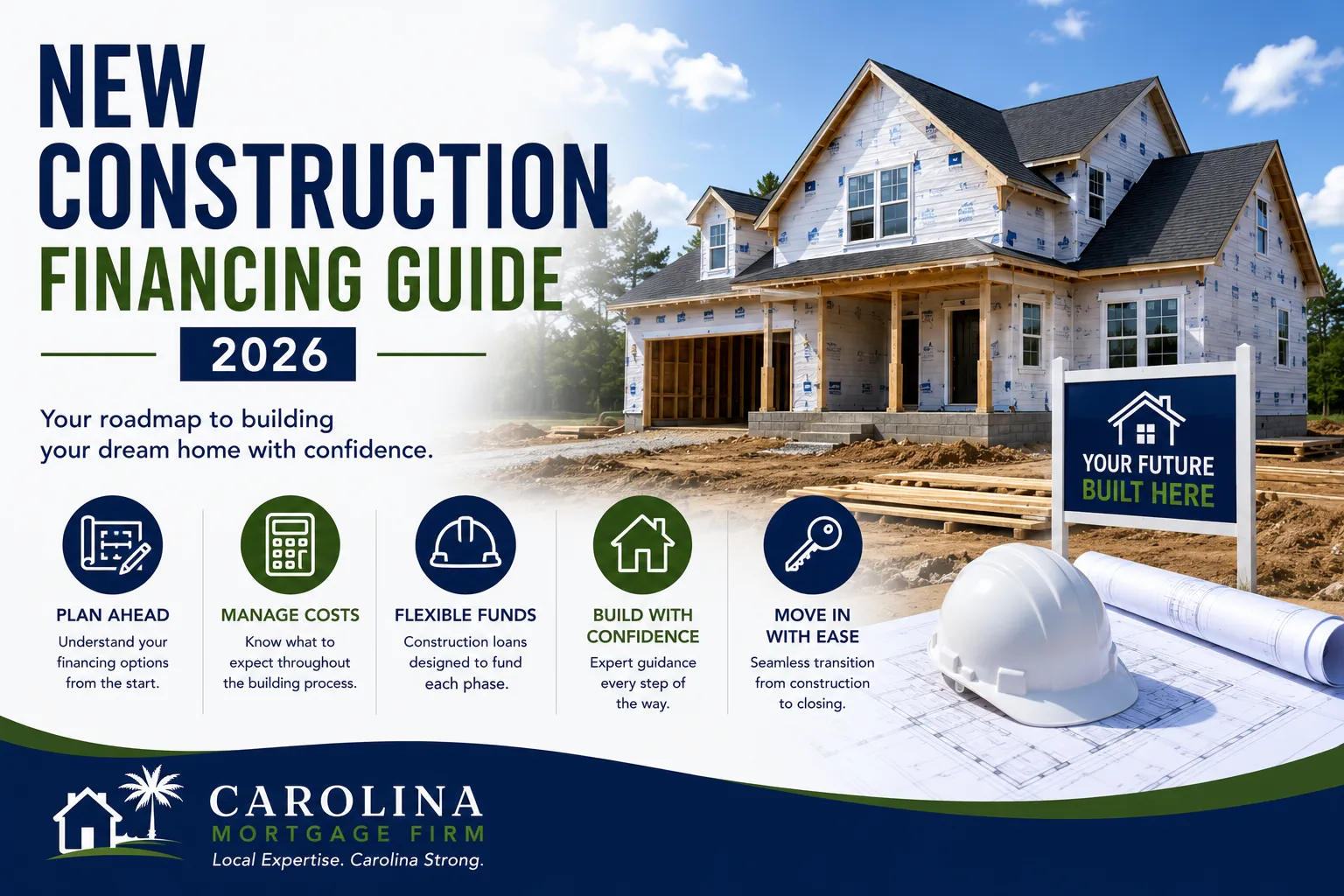

Building a brand-new home is an exciting experience. You get to choose your floor plan, select finishes, customize features, and move into a home that is designed specifically for your family’s needs. However, financing a newly constructed home is often different from purchasing an existing property. At Carolina Mortgage Firm, many buyers throughout Charlotte, Fort Mill, Indian Land, Rock Hill, Lancaster, Waxhaw, Matthews, and surrounding communities are surprised to discover that builder contracts, financing timelines, rate lock strategies, and closing costs can differ significantly from a traditional home purchase. Understanding these differences before signing a builder contract can save time, money, and frustration. Why Buyers Choose New Construction The Carolinas continue to experience tremendous population growth. As a result, builders are developing communities throughout: New construction remains attractive because buyers can often enjoy: Modern Floor Plans Today’s homes are designed around how families actually live. Open layouts, larger kitchens, home offices, and flexible living spaces continue to be popular. Energy Efficiency New homes often include: Builder Warranties Many builders provide warranties covering certain structural and mechanical components. Less Immediate Maintenance Everything is new, reducing the likelihood of major repairs during the first several years of ownership. How New Construction Financing Differs Many buyers assume financing a newly built home works exactly like financing an existing home. In some cases, that’s true. However, new construction transactions often involve additional considerations. Examples include: Understanding these variables is critical. Builder’s Preferred Lender: Should You Use Them? One of the first questions buyers encounter is: “Should I use the builder’s preferred lender?” The answer depends on the situation. Potential Advantages Builders frequently offer incentives such as: These incentives can provide significant value. Potential Disadvantages Sometimes buyers assume the builder’s lender is automatically the best financing option. That’s not always true. Buyers should compare: The goal is maximizing total value rather than focusing solely on incentives. Types of New Construction Financing Several financing options may be available. Conventional Loans Popular for buyers with strong credit and stable income. Benefits include: FHA Loans Often attractive for first-time buyers. Benefits include: VA Loans Eligible veterans may benefit from: USDA Loans Certain new construction communities may qualify depending on location. Understanding Builder Deposits Most builders require deposits during the construction process. Common deposits include: Earnest Money Submitted when signing the purchase agreement. Design Center Deposits Required when selecting upgrades and customizations. Additional Builder Deposits Some builders may require additional funds as construction progresses. These deposits are typically credited toward closing. However, buyers should understand refund policies before committing. Upgrades Can Impact Financing One of the most common mistakes buyers make is underestimating upgrade costs. Builder models often showcase: Many of these features are not included in the base price. It’s important to evaluate: Total Purchase Price Not just the advertised starting price. Monthly Payment Impact Upgrades increase financing needs. Budget Flexibility Avoid stretching finances beyond comfortable levels. Mortgage Rate Locks and New Construction New construction introduces unique rate lock considerations. Unlike existing homes that may close within 30-45 days, construction timelines often extend much longer. Common timelines include: Because of this, buyers should discuss: Extended Rate Locks Protection against future rate increases. Float-Down Options Potential ability to benefit if rates improve. Builder Incentive Programs Some builders offer financing-related promotions. Understanding these options early can prevent surprises later. What Happens During the Construction Process? The financing process generally follows several phases. Step 1: Pre-Approval Understand your budget before visiting builders. Step 2: Builder Contract Execute the purchase agreement. Step 3: Design Selections Choose upgrades and finishes. Step 4: Loan Processing Mortgage approval progresses while construction occurs. Step 5: Final Walkthrough Inspect the completed property. Step 6: Closing Finalize financing and receive keys. Planning ahead helps ensure a smoother experience. Common New Construction Mistakes Shopping Without Pre-Approval Many buyers visit builders before understanding their budget. Focusing Only on Incentives Builder incentives are valuable, but financing should still be compared. Underestimating Upgrades Model homes can create unrealistic expectations. Ignoring Future Expenses HOA fees, taxes, and insurance affect affordability. Waiting Too Long to Review Financing Early planning creates more options. Why Pre-Approval Matters Before Visiting Builders Obtaining a pre-approval first provides several advantages. Know Your Budget Understand what fits comfortably. Compare Builders More Effectively Evaluate communities within your price range. Avoid Disappointment Prevent falling in love with homes outside your budget. Strengthen Your Position Builders often take pre-approved buyers more seriously. Why Work With Carolina Mortgage Firm? At Carolina Mortgage Firm, we help buyers throughout: navigate the complexities of new construction financing. We compare: and help buyers evaluate builder incentives, financing options, and long-term affordability. Our goal is ensuring buyers make informed decisions before signing a builder contract. Frequently Asked Questions Do I Have to Use the Builder’s Lender? No. Are Builder Incentives Worth It? Often yes, but financing should still be compared. Can I Finance Upgrades? Typically yes, when included in the purchase contract. How Long Does Construction Take? Timelines vary by builder and community. When Should I Get Pre-Approved? Before visiting builders whenever possible. Related FHA Resources Ready to Build Your Dream Home? Whether you’re building in Charlotte, Fort Mill, Indian Land, Lancaster, Rock Hill, Waxhaw, or elsewhere throughout the Carolinas, Carolina Mortgage Firm can help you compare financing options and navigate the construction process with confidence. Contact our team today for a personalized mortgage consultation and pre-approval before visiting builders.

Buying Your First Home in North Carolina Purchasing your first home is one of the most exciting financial milestones you’ll ever achieve. It can also feel overwhelming. Between saving for a down payment, understanding mortgage options, comparing interest rates, and navigating the homebuying process, many first-time buyers aren’t sure where to begin. The good news is that homeownership may be more attainable than you think. Many buyers throughout Charlotte, Matthews, Mint Hill, Waxhaw, Concord, Huntersville, and surrounding North Carolina communities assume they need perfect credit and a 20% down payment to buy a home. In reality, there are numerous loan programs and assistance options available that can help qualified buyers purchase with much less money out of pocket. Understanding these programs can help you move from renting to owning sooner while building long-term financial stability. What Qualifies You as a First-Time Homebuyer? Many people are surprised to learn they may qualify as a first-time homebuyer even if they’ve owned a home before. Generally, a first-time homebuyer is someone who has not owned a primary residence within the previous three years. This definition allows many former homeowners who have been renting for several years to take advantage of first-time homebuyer benefits and assistance programs. The Biggest Myth About Buying a Home The most common misconception we hear is: “I need 20% down to buy a house.” This simply isn’t true for most buyers. Today’s mortgage market offers several options that require substantially less. Common Down Payment Options Loan ProgramMinimum Down PaymentConventionalAs low as 3%FHA3.5%VA0%USDA0% For many North Carolina buyers, qualifying for a mortgage isn’t the challenge. Understanding which loan program best fits their goals is often the bigger question. North Carolina First-Time Homebuyer Assistance Programs North Carolina offers several resources that may help qualified buyers reduce upfront costs. These programs can provide assistance with: Availability, income limits, and eligibility requirements vary based on location and individual circumstances. Because guidelines change periodically, it’s important to work with a knowledgeable mortgage professional who can identify available options. FHA Loans for First-Time Homebuyers FHA loans remain one of the most popular financing options for first-time buyers. Benefits of FHA Financing Lower Down Payment Qualified buyers can purchase with as little as 3.5% down. Flexible Credit Requirements FHA financing often accommodates borrowers whose credit profiles may not qualify for conventional financing. Gift Funds Allowed Family members can frequently assist with down payment funds through properly documented gifts. Higher Debt-to-Income Flexibility FHA guidelines may allow higher debt ratios than some conventional programs. For many Charlotte-area buyers, FHA financing provides an excellent pathway to homeownership. Conventional Loans for First-Time Buyers Conventional financing has become increasingly attractive because of its flexibility and competitive pricing. Advantages of Conventional Loans Borrowers with strong credit scores often find conventional financing to be one of the most cost-effective solutions available. VA Loans for Eligible Veterans North Carolina is home to a large military and veteran population. Qualified veterans and active-duty service members may benefit from: For military families throughout Charlotte and the surrounding region, VA financing remains one of the most valuable mortgage benefits available. USDA Loans in Eligible Areas Many buyers are surprised to learn that portions of North Carolina still qualify for USDA financing. Benefits include: Some communities outside major metropolitan areas may qualify for USDA financing while still offering convenient access to employment centers. How Much Home Can You Afford? Many buyers focus solely on the amount a lender can approve. A better question is: “How much home fits comfortably into my budget?” When evaluating affordability, consider: Buying at the top of your approval range isn’t always the best financial decision. Why Pre-Approval Should Be Your First Step Before viewing homes, obtaining a mortgage pre-approval should be your first priority. Benefits of Pre-Approval Understand Your Budget Know exactly what price range makes sense. Strengthen Your Offer Sellers often prefer buyers who have already completed financing reviews. Identify Potential Issues Early Income, asset, or credit concerns can be addressed before they become problems. Move Quickly In competitive markets, timing matters. Throughout Charlotte, Waxhaw, Matthews, Mint Hill, and Concord, pre-approved buyers often have a significant advantage. Common First-Time Homebuyer Mistakes Opening New Credit Accounts Avoid financing cars, furniture, or large purchases before closing. Changing Jobs Employment changes can affect loan approval. Moving Money Between Accounts Large undocumented transfers may require additional documentation. Ignoring Total Housing Costs Remember that taxes, insurance, HOA dues, and maintenance contribute to your monthly housing expense. Waiting Too Long to Talk With a Mortgage Professional Many buyers spend months looking at homes before understanding their financing options. Why Work With a Mortgage Broker? A mortgage broker provides access to multiple lenders rather than just one institution’s products. This often results in: At Carolina Mortgage Firm, we compare loan programs from multiple lenders to help buyers identify the best financing solution for their goals. Frequently Asked Questions Do I Need 20% Down? No. Many buyers purchase with as little as 3% to 5% down, while VA and USDA loans may allow zero down. What Credit Score Is Needed? Requirements vary by loan type, but options are available for a wide range of credit profiles. Can I Use Gift Funds? Yes. Many programs allow documented gift funds from family members. How Long Does the Mortgage Process Take? Most transactions close within 30 to 45 days, depending on the circumstances. Should I Get Pre-Approved Before Looking at Homes? Absolutely. Pre-approval helps establish your budget and strengthens your negotiating position. Related FHA Resources Link this article to: Ready to Buy Your First Home? Whether you’re purchasing in Charlotte, Matthews, Waxhaw, Mint Hill, Concord, Huntersville, or anywhere throughout North Carolina, Carolina Mortgage Firm can help you navigate the process with confidence. Our team specializes in helping first-time buyers understand their options, compare loan programs, and create a customized strategy that fits their financial goals. Contact Carolina Mortgage Firm today to get pre-approved and take the first step toward homeownership.

If you own rental property—or are planning to purchase one—you may be wondering: “Can I use rental income to qualify for a mortgage?” The answer is: Yes, in many cases rental income can be used to help qualify for a conventional mortgage. In fact, rental income is one of the most powerful tools available for increasing purchasing power and building long-term wealth through real estate. At Carolina Mortgage Firm, we help homeowners and investors throughout Charlotte, Fort Mill, Indian Land, Rock Hill, Lancaster, Matthews, Waxhaw, Belmont, Huntersville, and surrounding communities understand how lenders evaluate rental income and how it affects mortgage qualification. Let’s break down how conventional lenders calculate rental income and what you need to know before applying. Quick Answer: Rental Income Can Often Be Used to Qualify Conventional mortgage guidelines often allow borrowers to use rental income from: Existing Rental Properties Multi-Unit Properties New Investment Property Purchases Converted Primary Residences However, the income is not always counted dollar-for-dollar. Lenders generally apply specific calculations designed to account for vacancies, maintenance, and other real-world ownership costs. Why Rental Income Matters Rental income can significantly increase your borrowing power. For example: Without Rental Income: Annual Income: $90,000 With Rental Income: Annual Income: $90,000 Rental Income: $18,000 Total Qualifying Income: $108,000 This additional income may allow borrowers to qualify for: What Types of Rental Income Can Be Used? Several forms of rental income may be eligible. Existing Rental Property Income Income from properties already owned and rented. Multi-Family Property Income Income from duplexes, triplexes, and fourplexes. Boarder or Roommate Income Certain situations may allow consideration of boarder income. New Investment Property Income Projected rental income from newly purchased investment properties. Each category follows different documentation requirements. Rental Income From Existing Properties This is one of the most common scenarios. Lenders often review: Tax Returns Schedule E Forms Lease Agreements Current Rental History The goal is determining actual rental income generated by the property. Historical performance often plays an important role. What Is Schedule E? Schedule E is a section of your federal tax return used to report rental property income and expenses. Lenders frequently review: Gross Rental Income Property Expenses Depreciation Net Rental Income Because tax returns often include non-cash deductions such as depreciation, mortgage calculations may differ from taxable income calculations. This is why working with an experienced mortgage professional is important. Can I Use Rental Income From a Newly Purchased Investment Property? Often yes. For many conventional investment property purchases, lenders may use: Market Rent Estimates provided by the appraiser. The appraiser typically completes a rental analysis to estimate market rents for the property. This projected income may help support qualification. Rental Income and Multi-Unit Properties One of the most powerful opportunities available involves: Duplexes Triplexes Fourplexes Buyers may be able to occupy one unit while renting the others. Potential benefits include: Many first-time investors begin with multi-unit properties. What About Airbnb and Short-Term Rental Income? Short-term rental income has become increasingly popular. Examples include: The treatment of short-term rental income depends on: Because these situations can be complex, individual review is important. Why Lenders Don’t Count 100% of Rent One of the most common questions borrowers ask is: “Why can’t the lender use all of my rental income?” The answer is simple. Rental properties experience: Vacancies Maintenance Costs Repairs Turnover Expenses Lenders apply adjustments to account for these realities. This helps ensure borrowers can comfortably manage their mortgage obligations. Common Rental Income Mistakes Not Reporting Rental Income Properly Tax return documentation matters. Poor Record Keeping Incomplete records can create underwriting challenges. Assuming Gross Rent Equals Qualifying Income Mortgage calculations differ from landlord calculations. Waiting Until Contract to Review Qualification Investors should review financing options early. Rental Income vs Self-Employment Income Many real estate investors own properties personally while operating businesses separately. Lenders evaluate: Rental Income and Self-Employment Income under different guidelines. Understanding these distinctions can maximize qualification opportunities. Common Rental Income Myths Myth #1: Rental Income Doesn’t Count False. Rental income frequently helps borrowers qualify. Myth #2: Only Experienced Investors Can Use Rental Income False. New investors may qualify as well. Myth #3: Airbnb Income Is Always Ineligible False. Certain circumstances may allow consideration. Myth #4: One Rental Property Won’t Help False. Even modest rental income can increase purchasing power. How Rental Income Can Increase Buying Power Let’s look at an example. Borrower Income: $100,000 Annual Rental Income: $24,000 Total Qualifying Income: $124,000 This additional income may increase: Maximum Loan Amount Property Options Investment Opportunities Financing Flexibility Proper rental income analysis can make a substantial difference. Why Pre-Approval Matters Before purchasing an investment property—or using rental income to qualify—obtaining a pre-approval is essential. Benefits include: Accurate Income Analysis Loan Program Comparison Budget Planning Investment Strategy Development Faster Closings Many investors discover opportunities they didn’t realize were available. Why Work With Carolina Mortgage Firm? At Carolina Mortgage Firm, we help buyers and investors throughout: understand rental income guidelines and maximize their borrowing power. We compare: to identify the strategy that best supports your goals. Frequently Asked Questions Can Rental Income Be Used for a Conventional Loan? Often yes. Can I Use Income From an Investment Property I’m Buying? In many situations, yes. What Documents Are Required? Typically leases, tax returns, Schedule E forms, and appraisal reports. Can Airbnb Income Be Used? Possibly, depending on documentation and loan guidelines. Should I Get Pre-Approved Before Looking at Investment Properties? Absolutely. Related Conventional Resources Ready to See How Rental Income Can Increase Your Buying Power? Whether you’re purchasing your first duplex in Rock Hill, expanding a rental portfolio in Charlotte, investing in Fort Mill, or building long-term wealth in Lancaster County, Carolina Mortgage Firm can help you understand your financing options. Contact Carolina Mortgage Firm today for a personalized mortgage consultation and investment property review.