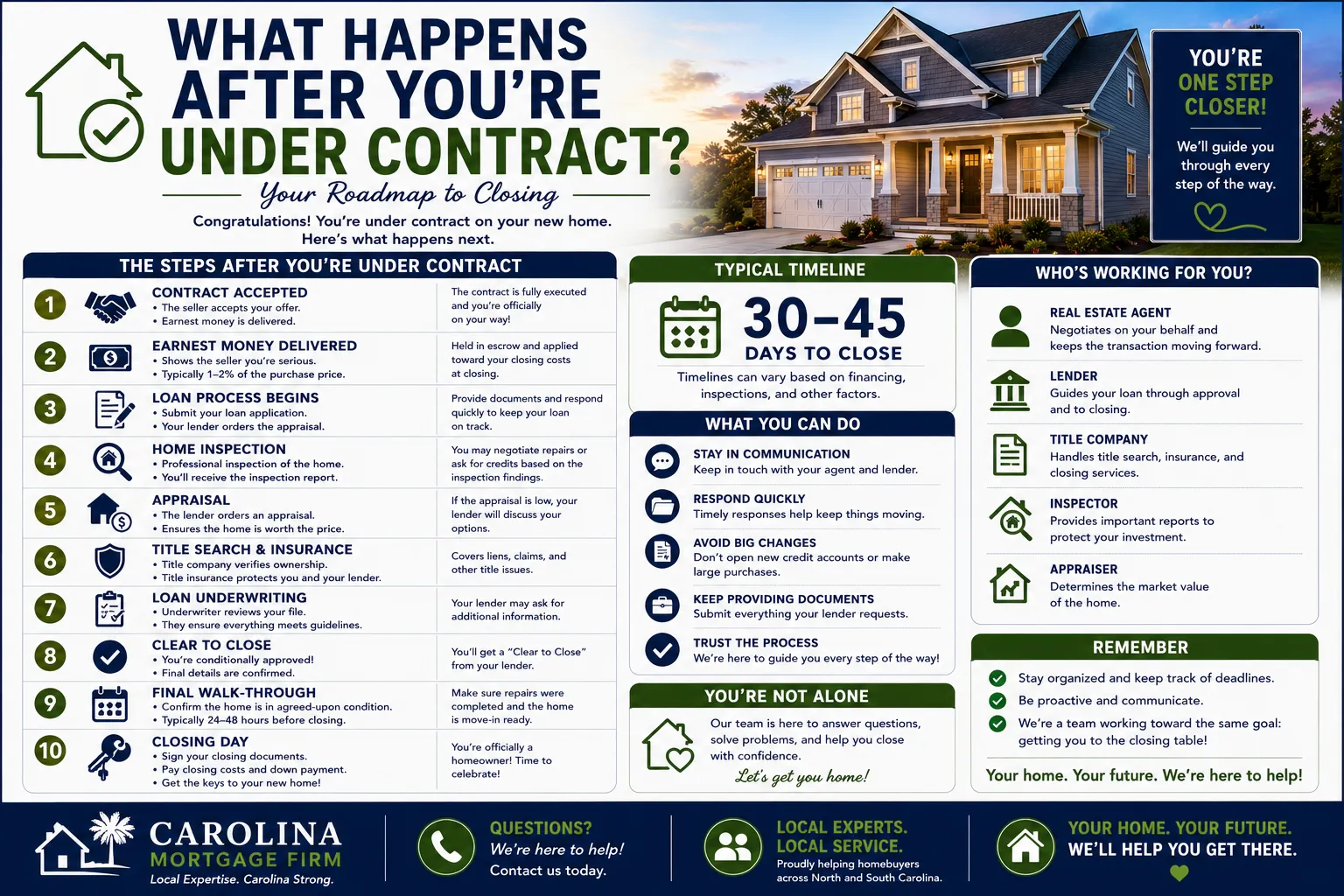

Congratulations!

Your offer has been accepted and you’re officially under contract on a new home.

This is one of the most exciting milestones in the homebuying journey, but it’s also where many buyers begin asking:

“Now what?”

At Carolina Mortgage Firm, we guide buyers throughout Charlotte, Fort Mill, Indian Land, Rock Hill, Lancaster, Waxhaw, Matthews, Belmont, and surrounding communities through this process every day.

While every transaction is unique, most home purchases follow a similar timeline from contract to closing.

Understanding what happens next can help reduce stress, avoid surprises, and ensure a smoother homebuying experience.

Step 1: Deliver the Contract

Once the purchase agreement is fully executed, your Realtor will typically provide the contract to all parties involved.

This often includes:

- Mortgage lender

- Closing attorney

- Buyer

- Seller

- Real estate agents

The mortgage process officially begins moving into full production.

At Carolina Mortgage Firm, we immediately begin reviewing the contract and preparing the file for underwriting.

Step 2: Update Your Mortgage Application

Even if you were already pre-approved, your loan file may need updates. Common items reviewed include:

Purchase Price

Ensuring the loan structure matches the final contract.

Closing Date

Confirming financing timelines.

Seller Concessions

Reviewing credits toward closing costs or rate buydowns.

Property Information

Updating address and property details.

These updates ensure your loan reflects the actual transaction.

Step 3: Initial Loan Disclosures

Federal regulations require borrowers to receive loan disclosures shortly after application. These documents outline:

- Loan terms

- Estimated closing costs

- Interest rate information

- Payment estimates

It’s important to review disclosures promptly and sign electronically when requested.

Delays at this stage can impact closing timelines.

Step 4: Home Inspection

Most buyers choose to complete a home inspection shortly after going under contract. A home inspection helps identify:

- Structural concerns

- Electrical issues

- Plumbing problems

- HVAC deficiencies

- Safety concerns

The inspection protects buyers by providing a better understanding of the property’s condition. While lenders generally don’t require inspections, they are highly recommended.

Step 5: Earnest Money and Due Diligence

Depending on your market and contract structure, you may have already submitted:

Earnest Money

Demonstrates your commitment to purchasing the property.

Due Diligence Funds

Common in North Carolina transactions.

Be sure to keep documentation showing these payments. Your lender may request copies during underwriting.

Step 6: Loan Processing Begins

Your file is assigned to processing.

The processor reviews documentation such as:

- Income

- Assets

- Credit

- Employment

- Property information

The goal is preparing the file for underwriting review.

During this stage, additional documentation requests are common. This is normal and should not cause concern.

Step 7: Appraisal Ordered

The lender typically orders an appraisal. The appraiser evaluates:

- Property condition

- Comparable sales

- Market value

The purpose is to ensure the property’s value supports the loan amount.

Most buyers are unfamiliar with the appraisal process, but it is a standard part of nearly every mortgage transaction.

Step 8: Underwriting Review

This is often the step that creates the most anxiety. The underwriter reviews:

Income

Verifies qualifying income.

Assets

Confirms funds available for closing.

Credit

Evaluates credit history and liabilities.

Property

Reviews appraisal and property documentation.

The underwriter’s role is ensuring the loan meets investor guidelines.

Step 9: Conditions

After reviewing the file, the underwriter may issue conditions. Common examples include:

- Updated bank statements

- Additional pay stubs

- Explanations for deposits

- Employment verification Receiving conditions is normal.

Almost every loan receives some form of conditional approval. Prompt responses help keep the transaction moving.

Step 10: Clear to Close

One of the best phone calls in the mortgage process is:

“You’re Clear to Close!”

This means:

- Underwriting requirements have been satisfied

- Final approval has been issued

- Closing documents can be prepared At this stage, you’re nearly at the finish line.

Step 11: Closing Disclosure

Borrowers receive a Closing Disclosure (CD) prior to closing.

The CD outlines:

- Final loan terms

- Interest rate

- Monthly payment

- Closing costs

- Cash needed to close

Reviewing the CD carefully is important.

Your mortgage advisor should be available to answer questions.

Step 12: Final Walkthrough

Shortly before closing, buyers typically complete a final walkthrough. The purpose is confirming:

- Agreed repairs were completed

- Property condition remains acceptable

- No unexpected issues exist This is not a second inspection.

It’s a final verification.

Step 13: Closing Day

Closing day has finally arrived. At closing, you’ll:

- Sign loan documents

- Review final paperwork

- Provide any required funds

- Receive ownership documentation

Once the transaction funds and records, you’re officially a homeowner. Congratulations!

Common Mistakes Buyers Make While Under Contract

Opening New Credit Accounts

Avoid financing furniture, appliances, or vehicles.

Changing Jobs

Employment changes can affect loan approval.

Moving Money Between Accounts

Large undocumented transfers can create underwriting questions.

Missing Document Requests

Responding quickly helps prevent delays.

Making Large Purchases

Avoid major financial changes until after closing.

How Long Does the Process Take?

Most transactions close within:

30 to 45 Days

However, timelines vary based on:

- Loan program

- Property type

- Appraisal timing

- Underwriting conditions

- Contract terms

Preparation and communication are key.

Why Work With Carolina Mortgage Firm?

At Carolina Mortgage Firm, we guide buyers throughout:

- Charlotte

- Fort Mill

- Indian Land

- Rock Hill

- Lancaster

- Matthews

- Waxhaw

- Belmont

- Concord

- Huntersville

through every step of the mortgage process. We provide:

- Weekly updates

- Clear communication

- Fast responses

- Multiple loan options

- Local expertise

Our goal is making the homebuying process as smooth and stress-free as possible.

Frequently Asked Questions

How Long Does Underwriting Take?

Typically a few days, though timelines vary.

What If the Appraisal Comes In Low?

Several options may be available depending on the circumstances.

Can I Buy Furniture Before Closing?

It’s usually best to wait until after closing.

What Does Clear to Close Mean?

Final underwriting approval has been issued.

When Do I Get the Keys?

Typically after the transaction funds and records.

Related Mortgage Resources

- Mortgage Pre-Approval Guide

- First-Time Homebuyer Programs

- FHA vs Conventional Loans

- How Much House Can I Afford?

- Mortgage Rate Lock Strategies

- Mortgage Broker vs Bank

Ready to Buy a Home?

Whether you’re purchasing your first home in Charlotte, moving to Fort Mill, relocating to Indian Land, buying in Rock Hill, or upgrading in Lancaster County, Carolina Mortgage Firm can guide you through every step of the mortgage process.

Contact our team today for a personalized mortgage consultation and pre-approval.