One of the biggest misconceptions in homeownership is that you need tens of thousands of dollars saved to buy a home.

In reality, many South Carolina homebuyers are surprised to discover they can purchase a home with significantly less money than they expected thanks to various down payment assistance programs and affordable mortgage options.

Whether you’re buying in Fort Mill, Rock Hill, Indian Land, Lancaster, York, Clover, Tega Cay, or elsewhere in South Carolina, understanding the available assistance programs can help make homeownership more attainable and less stressful.

For many buyers, the challenge isn’t qualifying for a mortgage. The challenge is saving enough money for the down payment and closing costs while also managing rent, student loans, childcare expenses, and everyday living costs.

Fortunately, South Carolina offers resources that can help bridge that gap.

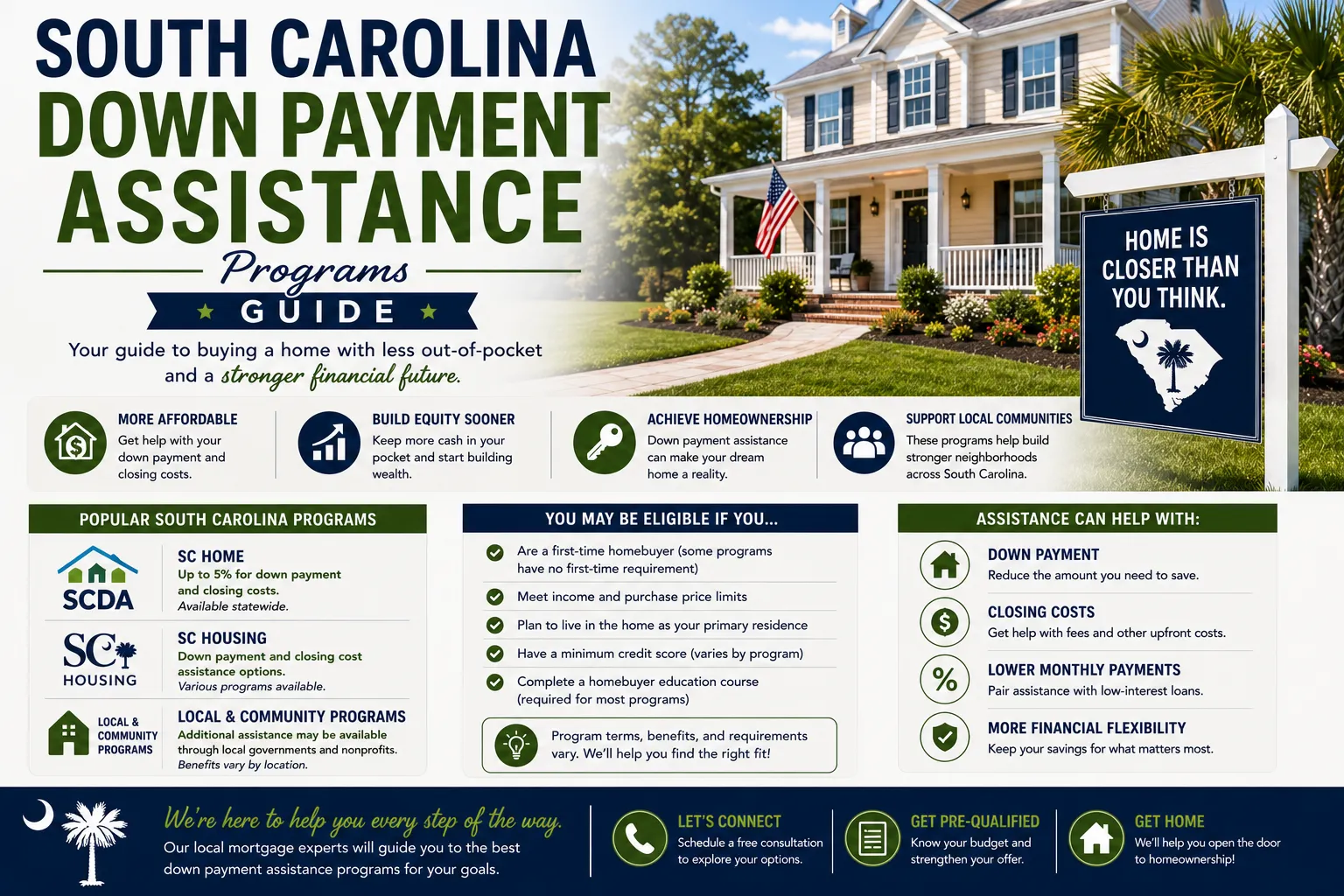

What Is Down Payment Assistance?

Down payment assistance programs are designed to help qualified buyers cover some or all of the upfront costs associated with purchasing a home.

These programs may provide assistance toward:

- Down payments

- Closing costs

- Prepaid taxes and insurance

- Homebuyer education programs

- Affordable mortgage financing

Depending on the program, assistance may be offered as:

- Grants

- Forgivable loans

- Deferred payment loans

- Low-interest second mortgages

Each program has its own eligibility requirements, income limits, and property restrictions.

Why South Carolina Buyers Use Down Payment Assistance

South Carolina continues to experience strong population growth, especially in communities near Charlotte. Areas such as:

- Fort Mill

- Indian Land

- Rock Hill

- Lancaster

- York

- Tega Cay

have become increasingly popular due to their proximity to Charlotte, lower property taxes, strong schools, and quality of life.

While these communities remain attractive, rising home values have made it more difficult for many first-time buyers to save enough cash for a home purchase.

Down payment assistance programs can help buyers enter the market sooner while preserving emergency savings and retirement funds.

SC Housing Programs

The South Carolina State Housing Finance and Development Authority (SC Housing) offers programs intended to help eligible buyers achieve homeownership.

These programs may provide:

Down Payment Assistance

Qualified buyers may receive assistance toward their down payment and closing costs.

Fixed Interest Rates

Many programs offer predictable fixed-rate financing.

Affordable Homeownership Opportunities

Programs are often designed to help moderate-income families purchase primary residences.

Program availability, income limits, and qualification requirements change periodically, so buyers should work with a knowledgeable mortgage professional to determine current eligibility.

FHA Loans and Down Payment Assistance

FHA financing remains one of the most popular options for first-time homebuyers. Benefits include:

3.5% Down Payment

Qualified buyers can purchase with a relatively small down payment.

Flexible Credit Requirements

FHA guidelines often accommodate borrowers with less-than-perfect credit.

Gift Funds Allowed

Family members can frequently assist with down payment requirements.

When combined with available assistance programs, FHA financing can significantly reduce the cash needed to purchase a home.

Conventional Financing Options

Many buyers assume down payment assistance only works with FHA loans. That’s not true.

Conventional financing may also be paired with certain assistance programs depending on program guidelines.

Benefits of conventional financing may include:

- Lower mortgage insurance costs

- Competitive interest rates

- Flexible loan terms

- Strong long-term affordability

For buyers with stronger credit profiles, conventional financing often provides excellent value.

USDA Financing in South Carolina

Many areas throughout South Carolina remain eligible for USDA financing. Benefits include:

Zero Down Payment

Qualified buyers may purchase with no down payment.

Competitive Rates

USDA loans often offer attractive interest rates.

Reduced Upfront Costs

Many buyers find USDA financing to be one of the most affordable homeownership options available.

Certain portions of Lancaster County and surrounding communities may qualify depending on property location and eligibility requirements.

Common Myths About Down Payment Assistance

Myth #1: The Program Is Only for Low-Income Buyers

Not always.

Many programs accommodate moderate-income households.

Myth #2: The Money Must Always Be Repaid

Some programs offer forgivable assistance.

Myth #3: The Process Is More Difficult

In many cases, the additional requirements are minimal.

Myth #4: Assistance Programs Take Longer

While additional documentation may be required, most transactions can still close within standard timeframes.

How Much Money Do You Actually Need?

The amount needed varies based on:

- Purchase price

- Loan type

- Property taxes

- Homeowners insurance

- Assistance program availability

- Seller concessions

Many buyers discover they need substantially less money than they originally assumed.

The best way to determine your actual cash-to-close requirement is through a mortgage consultation and pre-approval.

Why Pre-Approval Matters

Obtaining a mortgage pre-approval before shopping for homes provides several advantages.

Know Your Budget

Understand exactly what you can afford.

Identify Available Programs

Determine which assistance options may be available.

Strengthen Your Offer

Sellers prefer buyers who have already completed financing reviews.

Save Time

Address potential issues before finding a home.

In competitive communities such as Fort Mill and Indian Land, being pre-approved can make a significant difference.

Common Mistakes Buyers Make

Waiting Too Long

Many buyers delay speaking with a lender because they assume they need more savings.

Draining Savings Accounts

Maintaining emergency reserves is important even after purchasing a home.

Opening New Debt

New loans or credit cards can affect mortgage qualification.

Assuming They Won’t Qualify

Many buyers are surprised by the options available once they speak with a mortgage professional.

Why Work With Carolina Mortgage Firm?

At Carolina Mortgage Firm, we help buyers throughout:

- Fort Mill

- Indian Land

- Rock Hill

- Lancaster

- York

- Clover

- Tega Cay

- Charlotte Metro

understand their financing options and identify programs that may reduce upfront costs.

Because we work with multiple lenders, we’re able to compare loan programs and help buyers find solutions tailored to their specific goals.

Frequently Asked Questions

Do I Have to Be a First-Time Homebuyer?

Not always. Some programs are available to repeat buyers.

Can I Combine Assistance With FHA Financing?

Often yes, depending on program guidelines.

How Much Assistance Can I Receive?

Program limits vary and change periodically.

Will Assistance Affect My Interest Rate?

It depends on the specific program structure.

How Do I Find Out What I Qualify For?

The best first step is obtaining a mortgage pre-approval.

Internal Links

Link this article to:

- FHA Loans

- Conventional Loans

- USDA Loans

- First-Time Homebuyer Programs

- Mortgage Pre-Approval

- South Carolina Home Buying Guide

Ready to Buy a Home in South Carolina?

Whether you’re purchasing your first home in Fort Mill, moving to Indian Land, buying in Rock Hill, or relocating to Lancaster County, Carolina Mortgage Firm can help you understand your options and determine which programs may be available to reduce your upfront costs.

Contact our team today to get pre-approved and start your path toward homeownership.