If you’re paid on commission, you’ve probably wondered:

“Can I use my commission income to qualify for a mortgage?”

The answer is:

Yes, in many cases commission income can be used to qualify for a mortgage.

However, commission income is evaluated differently than salary or hourly income because it can fluctuate from year to year.

At Carolina Mortgage Firm, we help Realtors, loan officers, insurance agents, pharmaceutical sales representatives, car sales professionals, financial advisors, recruiters, and many other commission-based professionals throughout Charlotte, Fort Mill, Indian Land, Rock Hill, Lancaster, Matthews, Waxhaw, and surrounding communities successfully qualify for home financing.

Let’s explore how mortgage lenders evaluate commission income and what you can do to maximize your purchasing power.

Quick Answer: Commission Income Is Often Eligible

Most mortgage programs allow commission income when it can be properly documented and demonstrated as stable and likely to continue.

Lenders typically review:

Commission History

How long you’ve been earning commissions.

Income Stability

Whether earnings are reasonably consistent.

Employment History

Length of time in your profession.

Income Trends

Whether earnings are increasing, stable, or declining.

Because commission income varies from borrower to borrower, each file receives individual review.

What Is Considered Commission Income?

Commission income is compensation earned based on performance, sales volume, production, or revenue generation.

Examples include:

Real Estate Agents Mortgage Loan Officers Insurance Agents

Car Sales Professionals Financial Advisors Recruiters

Pharmaceutical Representatives Business Development Professionals

Many Charlotte-area professionals earn a significant portion of their compensation through commissions.

Why Lenders Evaluate Commission Income Differently

Unlike salary income, commission income may fluctuate. For example:

Year One: $75,000 Year Two: $110,000 Year Three: $95,000

Because earnings can vary, lenders must determine:

- Stability

- Continuance

- Average qualifying income

Their goal is ensuring borrowers can comfortably repay the mortgage over the long term.

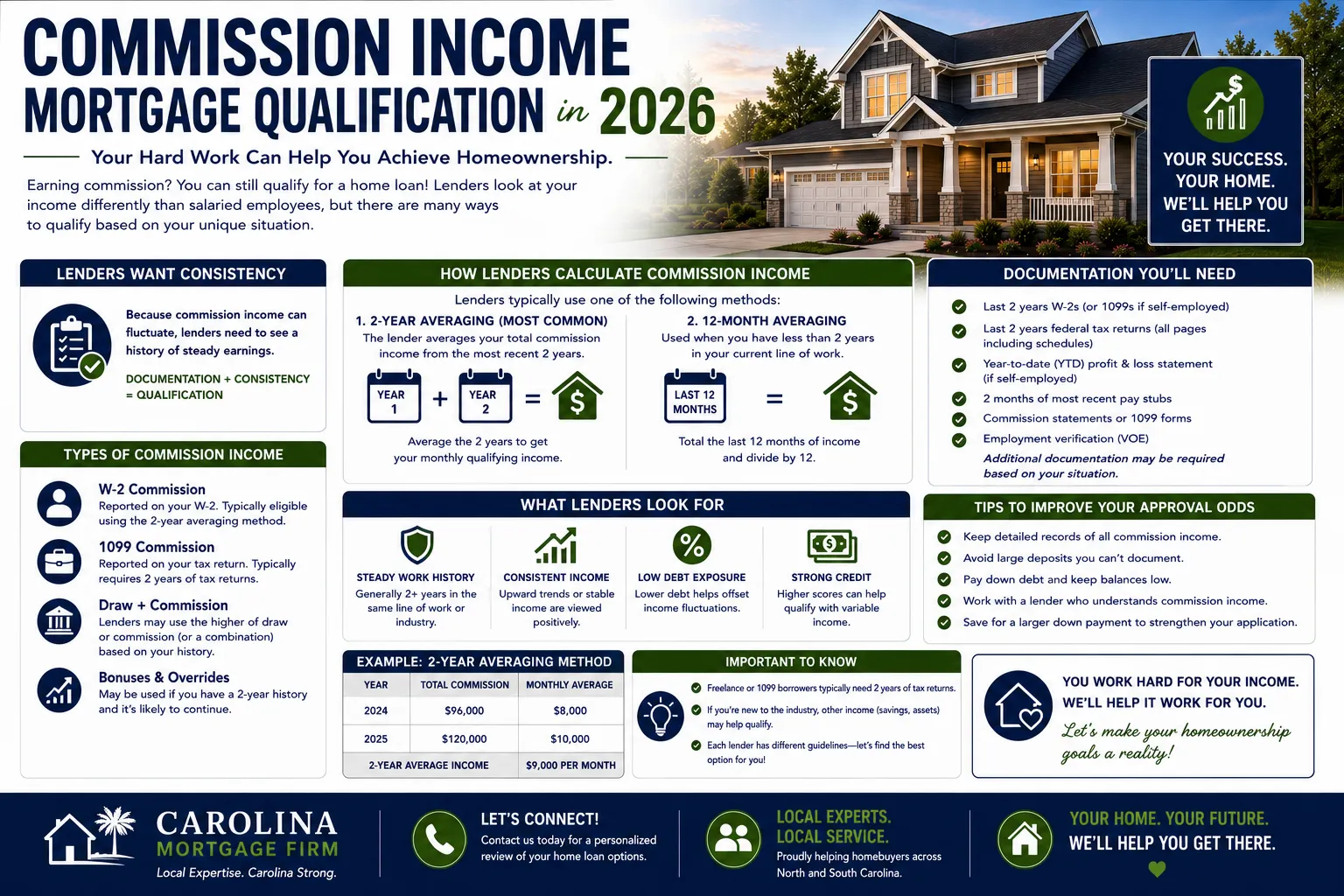

How Much Commission History Is Required?

In most cases, lenders prefer:

Two Years of Commission Income

A two-year history provides the strongest documentation.

However, this doesn’t necessarily mean less than two years automatically disqualifies a borrower. Factors such as:

- Prior industry experience

- Employment history

- Income stability may also be considered.

Every situation should be reviewed individually.

How Is Commission Income Calculated?

Lenders generally review historical earnings and establish an average.

For example:

Year 1: $90,000

Year 2: $110,000

Average Annual Income: $100,000 Monthly Qualifying Income: $8,333

The exact calculation depends on program guidelines and income documentation.

What Documents Are Required?

Commission income borrowers should expect to provide:

W-2 Forms Recent Pay Stubs Tax Returns

Year-to-Date Earnings Information

Additional documentation may be required depending on the percentage of income derived from commissions.

A mortgage professional can help determine exactly what is needed.

What If My Commission Income Is Increasing?

This is a common situation.

Many professionals experience growth as they advance in their careers. Examples include:

- Realtors building their client base

- Loan officers increasing production

- Sales professionals expanding territories

- Financial advisors growing assets under management

Increasing income trends are often viewed positively. However, lenders still evaluate sustainability and consistency.

What If My Income Varies Significantly?

Some variation is expected.

Many commission-based careers naturally experience:

- Seasonal fluctuations

- Market cycles

- Production swings

- Economic influences

The key is establishing a reliable long-term earnings pattern.

Mortgage guidelines are designed to account for reasonable fluctuations.

Commission Income and Self-Employment

Many borrowers confuse commission income with self-employment.

W-2 Commission Employee

Works for an employer and receives commissions.

Self-Employed Commission Earner

Operates independently or through a business entity.

The documentation and qualification process may differ significantly. Understanding your classification is important.

Can New Commission Income Be Used?

One of the most common questions we receive is:

“I recently switched to commission income. Can I still qualify?”

The answer depends on factors such as:

Previous Industry Experience Compensation Structure Employment History

Recent changes don’t automatically prevent qualification. However, additional review may be required.

Common Commission Income Myths

Myth #1: Commission Income Doesn’t Count

False.

Many borrowers qualify using commission income.

Myth #2: I Must Earn the Same Amount Every Year

False.

Income variation is expected.

Myth #3: Realtors Can’t Get Mortgages

False.

Thousands of Realtors obtain mortgages every year.

Myth #4: Commission Income Is Too Risky

Not necessarily.

Strong documentation and income history often support qualification.

How Commission Income Can Increase Buying Power

Many borrowers underestimate the impact of their commission earnings. For example:

Base Salary: $50,000

Average Annual Commission: $40,000 Total Qualifying Income: $90,000 Using all eligible income may increase:

Loan Eligibility Home Price Range Financing Flexibility Purchasing Power

A proper income analysis can make a substantial difference.

Why Pre-Approval Matters

If you earn commission income, pre-approval is one of the most important steps you can take. Benefits include:

Accurate Income Review

Determine what income may qualify.

Loan Program Comparison

Review Conventional, FHA, VA, and USDA options.

Budget Planning

Know exactly what you can afford.

Stronger Offers

Present a more competitive offer when you find a home.

Why Work With Carolina Mortgage Firm?

At Carolina Mortgage Firm, we regularly help commission-based professionals throughout:

- Charlotte

- Fort Mill

- Indian Land

- Rock Hill

- Lancaster

- Matthews

- Waxhaw

- Belmont

- Huntersville

- Concord

navigate mortgage qualification.

We understand the unique challenges associated with variable income and work with multiple lenders to identify solutions for:

- Realtors

- Loan Officers

- Insurance Agents

- Sales Professionals

- Financial Advisors

- Business Development Professionals

Our goal is helping you maximize your purchasing power while finding the right mortgage solution.

Frequently Asked Questions

Can Commission Income Be Used for a Mortgage?

Often yes.

How Much Commission History Do I Need?

Generally, lenders prefer an established history, often around two years.

Can Realtors Qualify for Mortgages?

Absolutely.

What Documents Are Required?

Typically tax returns, W-2s, pay stubs, and employment verification.

Should I Get Pre-Approved Before House Hunting?

Yes.

Related Conventional Resources

- What Credit Score Is Needed for a Conventional Loan?

- Can I Buy a Home With 3% Down?

- Can Bonus Income Be Used to Qualify?

- How Long Is a Mortgage Pre-Approval Good For?

- How Is Rental Income Calculated on a Conventional Loan?

Ready to See How Your Commission Income Impacts Your Buying Power?

Whether you’re a Realtor in Fort Mill, a financial advisor in Charlotte, an insurance agent in Rock Hill, a loan officer in Lancaster, or a sales professional anywhere throughout North or South Carolina, Carolina Mortgage Firm can help determine how your commission income fits into your mortgage qualification.

Contact Carolina Mortgage Firm today for a personalized mortgage consultation and pre-approval.