When you start shopping for a mortgage, one of the first decisions you’ll face is FHA vs. conventional. Both can get you into a home, but they work very differently — and choosing the wrong one could cost you money. At Carolina Mortgage Firm, we help buyers in South Carolina, North Carolina, Florida, and Louisiana understand exactly which loan fits their situation best.

What Is an FHA Loan?

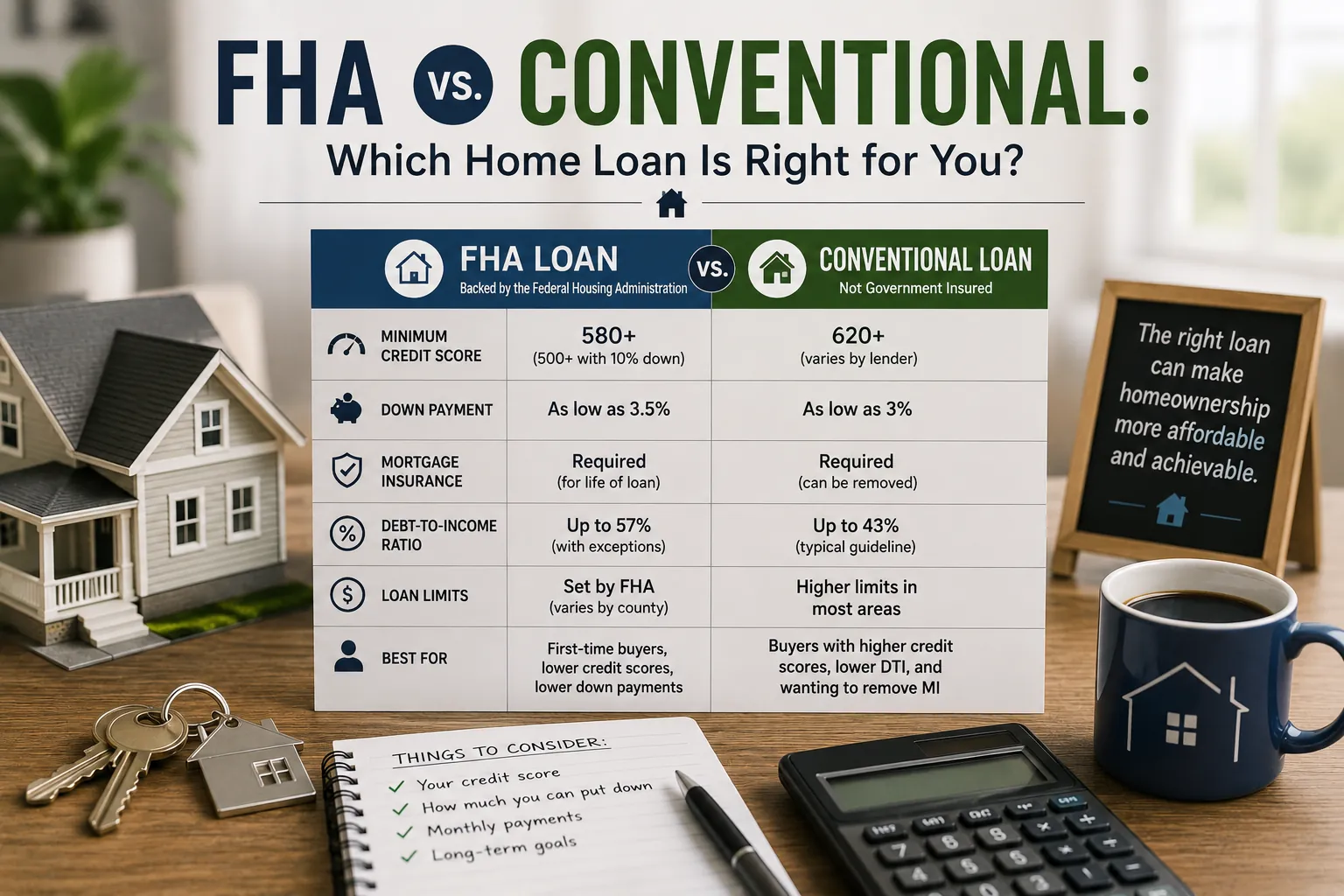

An FHA loan is backed by the Federal Housing Administration, which means the government insures the lender against losses if you default. Because of this guarantee, FHA loans allow lower credit scores (down to 580) and smaller down payments (as low as 3.5%). They’re an excellent option for first-time homebuyers or buyers who are still building their financial profile.

What Is a Conventional Loan?

A conventional loan is not government-backed — it’s issued and insured privately. Conventional loans require a higher credit score (typically 620+) and a slightly larger down payment (3-20%), but they offer more flexibility in loan limits, property types, and private mortgage insurance (PMI) rules. Conventional loans can often be the better long-term value for buyers with stronger credit.

Key Differences: FHA vs. Conventional

Down payment: FHA requires 3.5% (with 580+ credit); conventional starts at 3% but typically requires 5-10% for the best terms. Mortgage insurance: FHA charges a mandatory mortgage insurance premium (MIP) for the life of the loan in most cases. Conventional PMI drops off automatically when you reach 20% equity. Loan limits: FHA has county-by-county loan limits; conventional limits are higher in most markets. Property condition: FHA has stricter appraisal standards — the home must meet certain livability requirements.

When FHA Makes More Sense

Choose FHA if your credit score is below 680, if you have a limited down payment saved, if this is your first home purchase, or if you’ve had a past financial setback like a bankruptcy (FHA has shorter waiting periods).

When Conventional Makes More Sense

Choose conventional if your credit score is 700 or higher, if you can put 10-20% down, if you’re buying a higher-priced home near or above FHA limits, or if you want to avoid lifetime mortgage insurance. Sometimes buyers who qualify for FHA are actually better served by conventional — and we’ll always show you both options side by side.

Let’s Run the Numbers for Your Situation

The best loan is the one that saves you the most money and fits your life. At Carolina Mortgage Firm, we shop both FHA and conventional options — and more — to make sure you’re getting the best deal possible. Reach out today and let us find the right fit for you.