If you’ve owned your home for a few years, you may be sitting on more equity than you realize — and a cash-out refinance could be the smartest way to put it to work. Whether you’re remodeling your kitchen, adding a master suite, or upgrading your HVAC, Carolina Mortgage Firm helps homeowners in South Carolina, North Carolina, Florida, and Louisiana access their equity to fund the improvements they’ve been putting off.

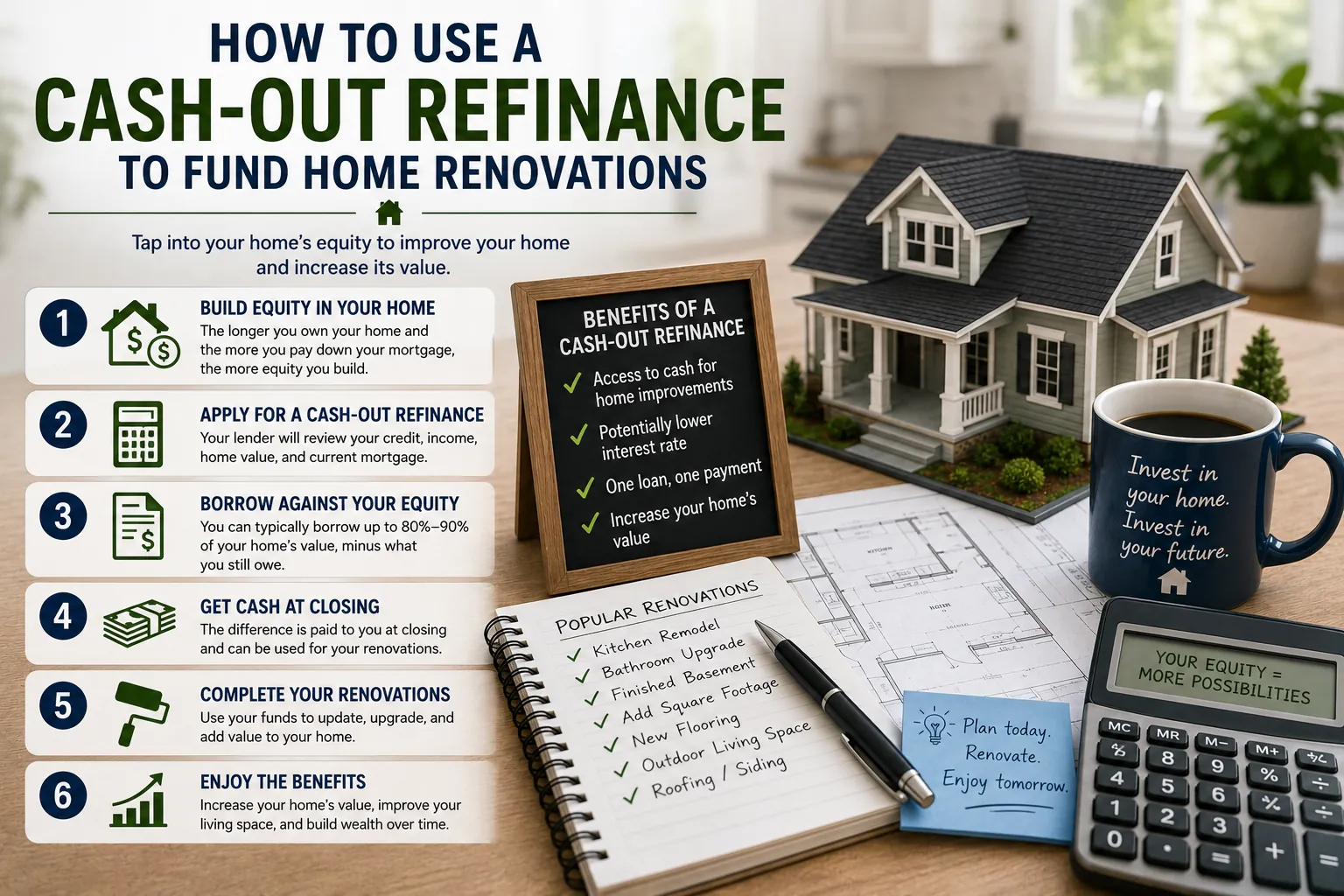

What Is a Cash-Out Refinance?

A cash-out refinance replaces your existing mortgage with a new, larger loan — and you receive the difference in cash at closing. For example, if your home is worth $350,000 and you owe $200,000, you have $150,000 in equity. A cash-out refinance might allow you to borrow up to 80% of the home’s value ($280,000), pay off your existing mortgage, and walk away with up to $80,000 in cash.

Why Use a Cash-Out Refi for Renovations?

Home renovation financing has several options — personal loans, home equity lines of credit (HELOCs), and credit cards among them. But a cash-out refinance often offers the lowest interest rate of any of them because the loan is secured by your home. Renovation projects that add value to your home are also a smart use of equity because they can increase what you’d earn when you eventually sell.

What Renovations Are Worth Financing?

Not all renovations are created equal when it comes to return on investment. Some of the highest-ROI projects include kitchen remodels, bathroom updates, adding usable square footage, energy-efficient upgrades (new windows, insulation, HVAC), and exterior improvements like new roofing or siding. We always recommend talking to a real estate professional about what improvements hold the most value in your specific local market.

What You’ll Need to Qualify

To qualify for a cash-out refinance, you’ll generally need at least 20% equity remaining in your home after the cash-out, a credit score of 620 or higher (640+ for better rates), a debt-to-income ratio below 43-45%, and documented income and employment. The process is very similar to your original mortgage application — we’ll review your full financial profile and find the best program for you.

Is a Cash-Out Refi Right for You?

A cash-out refinance makes the most sense when your current interest rate is close to or above today’s rates, when you need a significant lump sum for renovations, and when you plan to stay in the home long enough to recoup closing costs. If rates today are meaningfully higher than your current rate, a HELOC might be a better alternative — we’ll always show you multiple options.

Talk to Us Before You Start Swinging a Hammer

Before you commit to a renovation project or contractor, let’s talk about your financing options. At Carolina Mortgage Firm, we’ll review your equity position, run the numbers on a cash-out refi, and make sure you’re choosing the right tool for the job. Contact us today — your dream renovation might be closer than you think.